Q & A

Joining the Pension Fund

In terms of my pension fund, what do I need to consider when I start a new job?

- If your gross annual salary exceeds the entry threshold (in most cases CHF 22,050, although it may be lower depending on your employer’s pension solution), your new employer must register you with Nest.

- As a next step, you will receive a letter entitled «Invitation Connect¦Members».

- Please use the code provided in the letter to register on the Connect portal for members on our website connect.nest-info.ch. Once registered, you can access your insurance certificate and your employer’s pension plan in your mailbox.

- Please check your insurance certificate, in particular your date of birth, your marital status and the gross annual salary registered with us (which is your contractually agreed gross monthly salary, calculated over a full year, i.e. multiplied by 12 or 13)

- Your employer will send you a form entitled -> ‘Deklaration Freizügigkeitsleistung’ und ‘Zahlungsauftrag für die ehemalige Vorsorgeeinrichtung’ (‘declaration of vested benefits’ and ‘payment order for the previous pension fund’). On page 2 of this form, you instruct your previous pension fund to transfer your vested benefits to Nest. On page 1 of the form, you notify Nest whether you have any vested benefits and which pension fund will be transferring them to Nest.

If you have not received the form, you can access it in your Connect mailbox in the ‘Messages’ folder, or on the Nest website.

Further information is available in the Pension Fund Regulations of January 2024, Art. 8, Art. 12, and others.

How can I confirm that my assets have been transferred from my previous pension fund?

- Your previous pension fund should have sent you a termination statement.

- Once your vested benefits have been credited to your personal account with Nest, you will receive an e-mail informing you that you have a new insurance certificate in your Connect mailbox. The insurance certificate will show the amount of vested benefits transferred and credited to your account under item 4 ‘Deposits’.

Further information is available in the Pension Fund Regulations of January 2024, Art. 21, Art. 24, and others.

Why do I have to fill in the health declaration form?

- Depending on your salary and age, Nest may require information about your state of health if you start a new job with an employer whose pension plan provides for a high level of insured benefits.

- Moreover, Nest may require a health declaration in the event of a salary increase, an amendment of the pension plan or a switch to a different plan.

- In the event of non-cooperation or high risk, Nest may issue a reservation (Gesundheitsvorbehalt [health reservation]).

Further information is available in the Pension Fund Regulations of January 2024, Art. 14, Art. 15, and others.

Change in salary

My salary has been raised – will this affect my pension fund?

- Yes, an increase in the gross annual salary normally entails an increase in the insured benefits and contributions.

- Your employer is obliged to notify Nest of any salary changes of 10% or more to ensure that your employee benefits will be adjusted accordingly.

- Once we have processed this change, you will receive an e-mail informing you that you have a new insurance certificate in your Connect mailbox which specifies your new benefit and contribution figures.

- Please check your insurance certificate, in particular your date of birth, your marital status and the gross annual salary registered with us (it equals your contractually agreed gross monthly salary, calculated over a full year, i.e. multiplied by 12 or 13).

Further information is available in the Pension Fund Regulations of January 2024 under Art. 16.

My employer has agreed to increase / reduce my working hours – will this affect my pension fund?

- Yes, if the change in working hours is associated with a change in salary, this will normally entail an increase/reduction in insured benefits and contributions.

- Your employer is obliged to notify Nest of any salary changes of 10% or more to ensure that your employee benefits will be adjusted accordingly.

- Once we have processed this change, you will receive an e-mail informing you that you have a new insurance certificate in your Connect mailbox which lists your new benefit and contribution figures.

- Please check your insurance certificate, in particular your date of birth, your marital status and the gross annual salary registered with us (which is your contractually agreed gross monthly salary, calculated over a full year, i.e. multiplied by 12 or 13).

Further information is available in the Pension Fund Regulations of January 2024, Art. 16.

Buy-in into the Pension Fund

What does ‘buy-in into the pension fund’ mean and how do I go about it?

- Buying into the Pension Fund means reducing or closing benefit shortfalls, primarily in terms of your retirement benefits. A shortfall may arise if, for instance, your employment was interrupted, your savings process under the employee benefits scheme was discontinued for a time, or your current employer has a pension plan with higher savings rates (see pension plan). A salary increase can also lead to a shortfall in benefits.

- A buy-in reduces your tax bill, since buy-ins into the pension fund can be deducted in full from your taxable income (after each buy-in Nest will send you a tax confirmation by post, which must be submitted to the tax office).

- Buy-ins can be made at any time and several times a year.

- The maximum buy-in amount is equal to the difference between the accrued retirement assets and the maximum reachable retirement assets. The latter correspond to the assets you would have reached if you had been insured under the current pension plan on the current salary since the start of the savings process.

- To check whether you have a benefit shortfall (and can therefore make a buy-in) and find out your potential buy-in amount, please refer to item 8 of your current insurance certificate in your Connect mailbox.

- Please contact your customer advisor at Nest for the required documents.

Further information is available in the ‘Einkauf’ (buy-in) leaflet and the Pension Fund Regulations of January 2024, Art. 21.

Unpaid leave

I am planning to take unpaid leave – how will this affect my benefits?

- In the event of unpaid leave (1 - 12 months), Nest offers three different options:

a) savings process and risk insurance continue as before

b) savings process is suspended and risk insurance continues (death, disability)

c) both the savings process and risk insurance (death, disability) are suspended

- If you choose option 1 or 2, your employer may invoice you for the total costs, i.e. the employee AND employer contributions (see current insurance certificate, item 4) for the duration of your unpaid leave. Please note that we recommend arranging interim accident insurance or private accident insurance.

Please note that the form must be signed by both you and your employer and submitted to Nest before the start of unpaid leave.

Further information is available in the Pension Fund Regulations of January 2024, Art. 10 para. 1.

Marriage

When I get married, what do I need to do regarding my employee benefits insurance?

- We recommend that you notify your employer when you get married. The employer will then send us the relevant form so that we can record your new marital status.

- Alternatively, you can write to us directly to notify us of your change of marital status. Please enclose a copy of an official letter stating the new surname, marital status and date of marriage (e.g. civil status certificate, family certificate, registered partnership certificate).

- Note: Once we have entered your new marital status in our system, the Nest Collective Foundation will send you a letter by post stating the amount of your retirement assets at the time of marriage. This document is particularly important in the event of a divorce.

Further information is available in the ‘Heirat’ (marriage) leaflet and the Pension Fund Regulations of January 2024, Art. 6, Art. 34 ff., and others.

Cohabitation

I live in a marriage-like relationship and would like to recognise my partner as a beneficiary, what do I have to do?

- If you live in a marriage-like relationship but are neither married nor in a registered partnership, your partner has the same entitlements as married partners if he/she

a) is responsible for the maintenance of at least one child who was under your joint care before the death or

b) one of the two following conditions is met:

1) you were living with your partner in the same home for the last five years before your death or

2) you have provided Nest with a cohabitation agreement signed by you and your partner during your lifetime

Further information is available in the ‘Konkubinat’ (cohabitation) leaflet and the Pension Fund Regulations of January 2024, Art. 34, Art. 38, Appendix.

Divorce

What steps do I have to take when I get divorced?

- Your solicitor or competent court will send a request regarding the initiation of divorce proceedings either to you or to us in our capacity as your pension fund. We will respond by sending a pension compensation statement (so-called feasibility check declaration). The court will use this document to transfer part of your pension assets to your former spouse.

- As soon as the vested benefits have been credited or debited from your personal account at Nest, we will send you an e-mail to inform you that a new insurance certificate is available in your Connect mailbox. This certificate shows the amount of the vested benefits credited or debited under item 4 ‘Payments’ or ‘Withdrawals’.

- A divorce repayment can be made at any time – as a rule before any employee buy-ins.

Further information is available in the Pension Fund Regulations of January 2024, Art. 53, Art. 54.

Promotion of home ownership

I would like to use money from my retirement savings to buy a home. How do I proceed?

- You can find the maximum advance withdrawal amount under item 8 of your current insurance certificate in your Connect mailbox.

- The minimum advance withdrawal is CHF 20,000 (in the same pension fund, you can only make an advance withdrawal every five years). If the money is used to buy into a housing cooperative (purchase of share certificates), there is no lower limit.

- The property in question must be your main residence and you must live there yourself. Second homes or retirement homes abroad are not eligible (a special assessment is made for residential property abroad, e.g. for properties close to the border).

~ Steps to take:

- As a rule, you will discuss this matter with your bank or notary.

- Once you contact us with your specific ideas, we will send you documents to fill out, sign and return to us, along with all the required enclosures, so that we can review your application.

- If all the conditions are met, a transfer can be made to a frozen, special-purpose account.

- We will notify the relevant tax authority (if you are resident abroad, the applicable withholding tax will be deducted directly from the transfer amount).

Further information is available in the ‘Promotion of home ownership’ leaflet and the Pension Fund Regulations of January 2024, Art. 55 as well as the Reglement über Wohneigentumsförderung mit Mitteln der beruflichen Vorsorge (WEF) (Regulation on the Promotion of Home Ownership using Pension Fund Assets).

Incapacity for work / disability

Will I receive benefits from the pension fund if I am partially or fully incapacitated for work due to illness (or accident)?

- Your employer is obliged to notify the Nest Collective Foundation or PKRück of your partial or complete incapacity for work one month after its onset, using the ‘Meldung Arbeitsunfähigkeit’ (notification of incapacity for work) form (pages 1 and 2). Please complete pages 4 and 5 personally and send them to PKRück.

- If the criteria for the provision of benefits are met, there will be an exemption from contributions, i.e. from day 91 onwards lower or no contributions will be payable by your employer. During these periods, and to the extent of your incapacity for work, this means that your payslip may only show lower BVG contributions or none at all. However, even if you leave the company, Nest will continue to accrue your retirement savings account until you have fully recovered or reached the normal retirement age. If the incapacity for work results in disability, your entitlement to a disability pension from the Nest Pension Fund will be assessed on the basis of an IV decision (6 months’ notice). Any disability pension is based on the annual salary insured at the start of the incapacity for work.

Further information is available in the Pension Fund Regulations of January 2024, Art. 39 ff.

Death

What happens to my pension insurance when I die?

- Your employer is obliged to notify Nest of the death of any members.

- Nest will assess any entitlement to survivors’ benefits (e.g. partner’s pension, orphan’s pension) on the basis of the current Pension Fund Regulations and the applicable pension plan.

- Surviving dependants must register their claim with Nest within 3 months of the death of the member.

Further information is available in the Pension Fund Regulations of January 2024, Art. 33 ff.

Departure from the Nest Collective Foundation

What steps will I have to take when my employment contract ends?

- Once we receive an Austrittsmeldung (notification of your departure) from your employer, we will send you the ‘Freizügigkeitsanspruch’ (vested benefits entitlement) form by post. Please complete this form to specify where your vested benefits should be transferred to.

Note: We may also send you the ‘Freizügigkeitsanspruch’ (vested benefits entitlement) form if your gross annual salary falls below the entry threshold specified in the pension plan. - If your new employment is already confirmed and you have notified us in writing of your new employer’s pension fund, we will transfer your entire vested benefits to the new pension fund.

- If you don’t have a new employer or pension fund yet, you have to set up a vested benefits account or a vested benefits policy with a vested benefits foundation, a bank or a life insurance company.

- If you were insured with Nest for at least one year and are not starting a new job after leaving, you have the option of continuing your employee benefits insurance with Nest for a maximum of two years in the form of a voluntary individual insurance policy.

- Under certain circumstances, you may also receive your vested benefits in cash.

Further information is available in the ‘Barauszahlung von Guthaben aus der beruflichen Vorsorge bei definitivem Verlassen der Schweiz’ (cash payment of pension fund assets on permanent departure from Switzerland) leaflet and in the Pension Fund Regulations of January 2024, Art. 10 para. 3, Art. 4, Art. 49 ff.

Continued insurance in the event of termination by the employer after the age of 58

What are my options if I lose my job and am at least 58 years old?

- If your employer notifies us that they have terminated your employment and will deregister you from the employee benefits scheme, you have the option of continuing your employee benefits insurance with the Nest Collective Foundation pursuant to Art. 47a BVG.

- Nest will send you a form by post which you can use to apply for continued risk insurance cover for the events of death and disability and/or for pension insurance cover (savings process). The application must be received by us within one month.

Further information is available in the ‘Weiterversicherung für Versicherte’ (continued insurance for members) leaflet and in the Pension Fund Regulations of January 2024, Art. 11.

Retirement

How will the Nest Collective Foundation know when I want to retire?

- Around 6 months before you reach the reference age (previously: ‘regular retirement age’), Nest will send you the relevant form by post. Please use this form to let us know how you would like to draw your retirement benefits – pension, lump sum or both.

- Early retirement: Full or partial early retirement always requires a respective discontinuation of gainful employment.

- Once you reach the age of 58, you can take full or gradual retirement in a maximum of three stages (at least a 20% reduction in working hours or salary and at least one year between any two stages).

- Deferred retirement: With your employer’s consent, you can continue to work beyond the reference age (previously: regular retirement age) until you reach the age of 70. The employer is responsible for paying at least 50% of the contributions. Risk insurance contributions no longer have to be paid after the reference age.

- From the age of 50, you can also buy into early retirement, i.e. in the event of early retirement you will receive (at most) the same retirement benefit as if you had continued working up to the reference age.

Further information is available in the ‘Pensionierung’ (retirement) leaflet and in the Pension Fund Regulations of January 2024 as well as in Art. 17 (Weiterversicherung des bisherigen Lohnes ab Alter 58 [continued insurance of the previous salary from age 58]), Art. 22 (Einkauf in die vorzeitige Pensionierung [buy-in into early retirement]), Art. 24 ff.

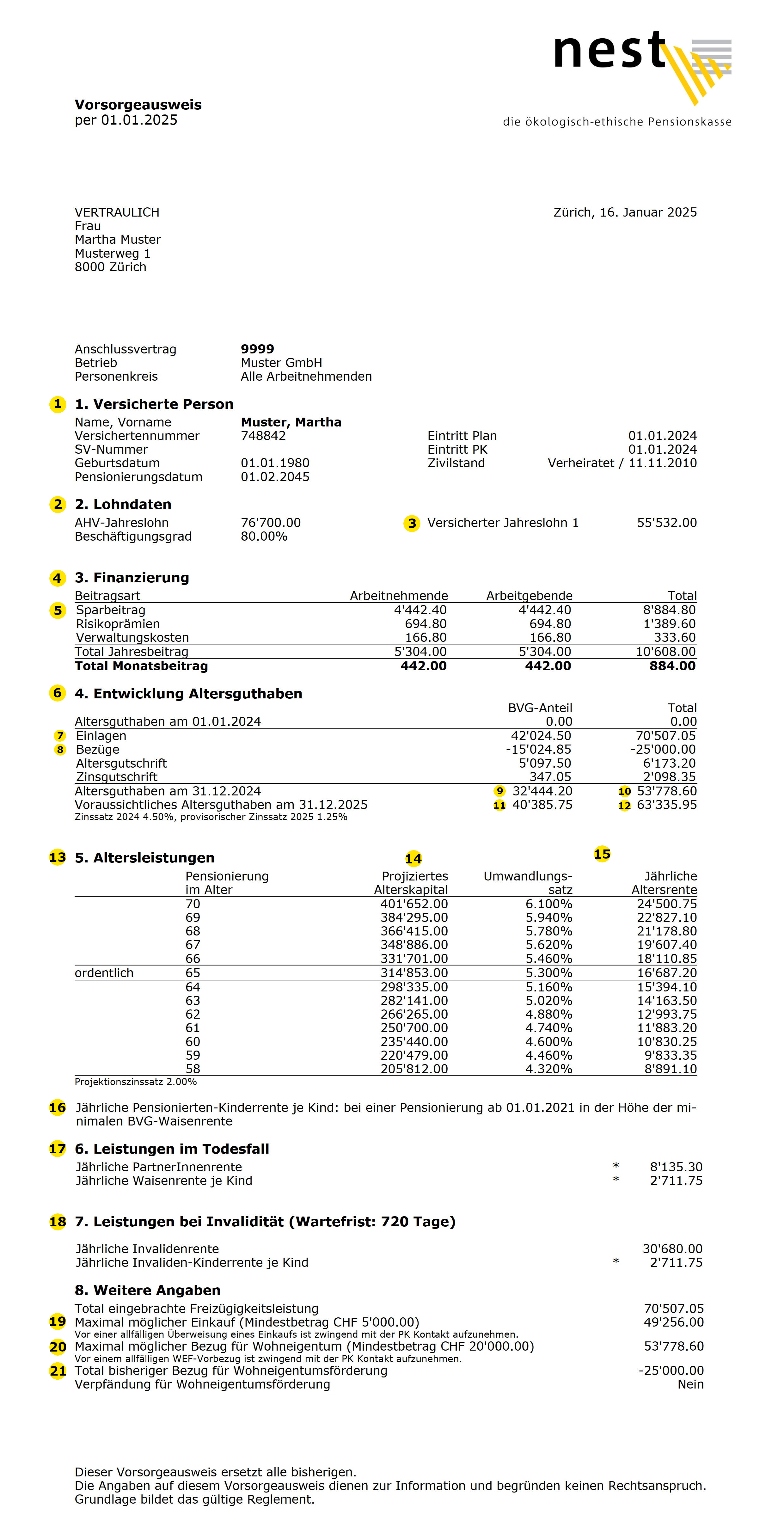

Insurance certificate

What role does the insurance certificate play?

The insurance certificate is filed in your Nest Connect mailbox at the start of your employee benefits insurance and whenever there is a change, such as the inclusion of vested benefits, buy-ins, salary changes, annual reporting, etc. The certificate specifies the amount of your insured benefits in the event of disability, death and old age (projected) and the amount of the premiums or contributions we charge to your employer. These contributions depend on your gross annual salary, your age and the structure of your pension plan.

Important: Please check that the amount deducted on the payslips from your employer matches your monthly contribution under item 3 of your insurance certificate.

You can find more information in the following places:

- On the page Aktivversicherte under “Mein Vorsorgeausweis”

- Sample pension certificate

- Explanation of the pension statement

{kind=link}

Pension plan

What role does the pension plan play?

The pension plan is filed in your Connect mailbox at the start of your employee benefits insurance and then once a year on 1 January yyyy. The plan specifies the pension solution that your employer has chosen for the employees. The Federal Law on Occupational Retirement, Survivors’ and Disability Pension Plans (BVG) sets out minimum requirements for the structure of the pension plan (e.g. savings rates of 7%/10%/15%/18% of the coordinated annual salary); however, the employer is free to raise these rates for the employees, e.g. to 8%/11%/16%/19%, which will result in higher savings assets and higher retirement benefits. It is also possible to insure higher disability or death benefits.